I'm Matt Bashar Whitney retreat calm here in New York City for a week. 2015, I'm joined by Bob Connolly, a finance professor with the University of North Carolina in Chapel Hill. Bob, thanks so much for joining. Thanks rather than now, can investors in reindex products assume efficient market pricing? And if so, does the same hold true for individual rates? It's a good question. So the answer is, for a long time, we've been very clear that indexes are very efficiently priced. So what we've been doing is asking the question at the level of an individual Reed. Could investors expect that the price discovery process was really working literally in the sort of textbook manner? And the answer from our work is, it looks very much like the average read works extraordinarily well in this respect. We've got a few now and again, where the efficiency isn't all we look for from a theoretical perspective, but the cool part that we thought we found in our work is the market seems to fix itself. So a read that has a tough quarter in terms of the price discovery process, they tend to bounce back very rapidly. So from an investor's perspective, I think they can take it as an article of faith the average read, in fact, just about every read, is going to be efficiently priced every single period. And what factors contribute to the efficiency of an individual is an interesting question. So there is some literature that suggests that institutional ownership plays a big role. And in fact, what we discovered is not only to institutional owners play a big role, but it's the long-term slow traders that actually are the most crucial for understanding efficiency process. That is, it's not the trader, the...

Award-winning PDF software

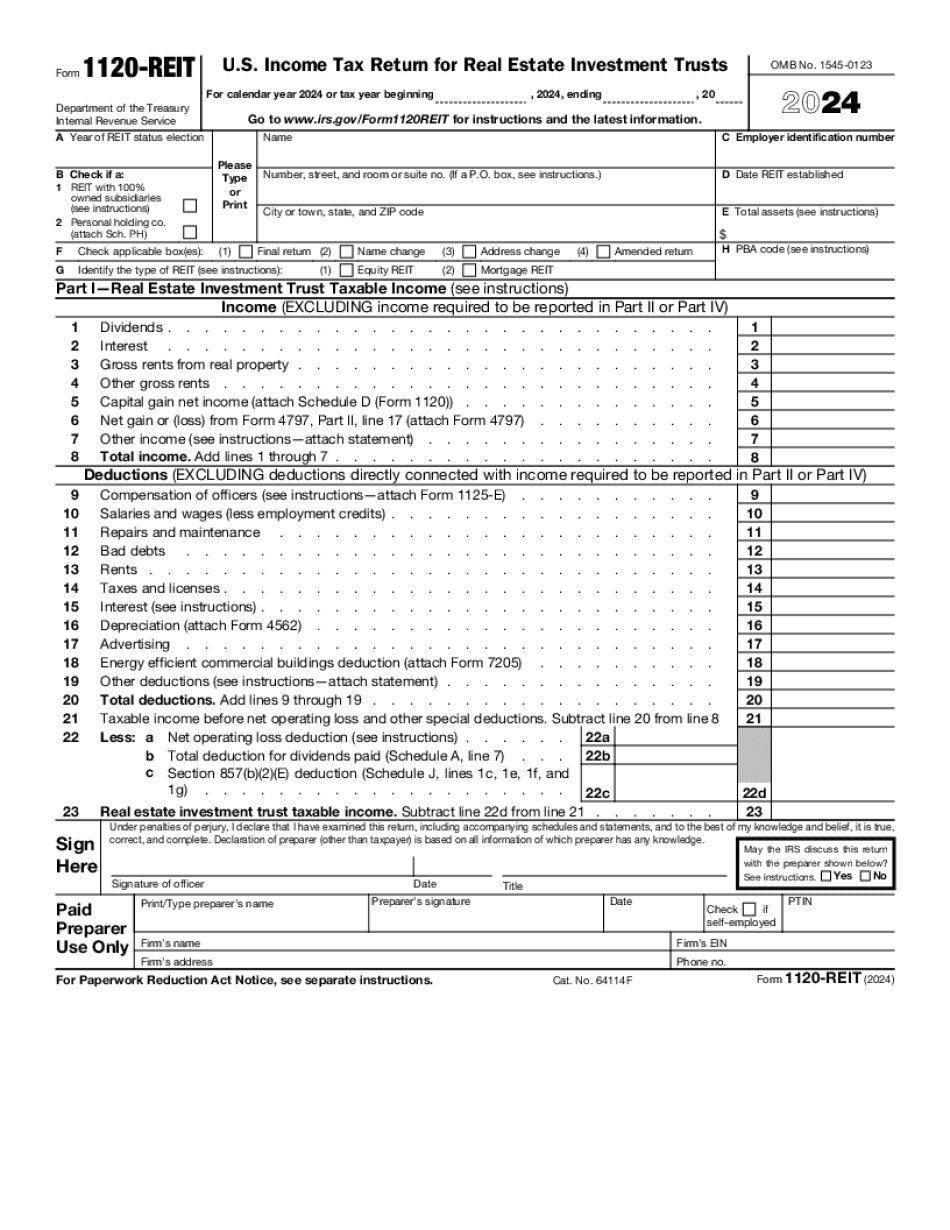

Video instructions and help with filling out and completing Why Form 1120 Reit Indexes